How measure the impact of construction amnesty?

It is improbable if not impossible to measure the impact from publicly available data

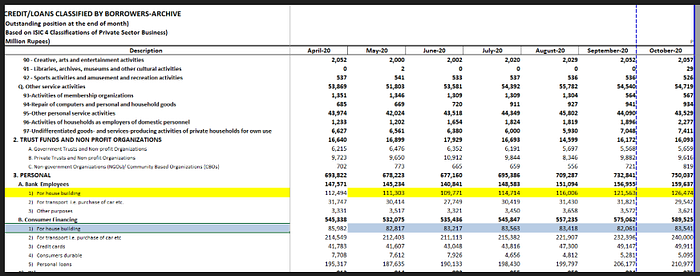

All of us are looking forward to the construction sector taking off and adding to the GDP and employment generation in the country. The purpose of this post is to show how difficult it is to measure the construction activity in the country based on the publicly available data. The below analysis was published in Business Recorder two days ago implying 28 billion of construction activity took place due to construction package in last three months.

Aqeel Karim Dhedhi, Gohar Ijaz, Hasan Bakhshi and Kamran Khan have already declared it “best amnesty in the history of the country”, “a game changer”, and a “development second in significance only to independence of the country.” Kamran Khan has done number of programs and Vlogs on the amnesty and if you can’t bear to listen to it, I have done two threads with show notes. You can click on the below tweet and peruse the show notes to see the key points presented by the host and the guests. However, I recommend you at least listen to Kamran Khan’s monologue which uplifts the mood, spirit and morale of the viewer by listing all the ways the package will lead to the uplift of the country.

Why should we measure the impact of the amnesty? Measuring the impact of construction package will enable us to learn what worked, why it worked and help us design better amnesty schemes in the future. The post is divided into 7 sections. The first section summaries the construction packages. The second section gives a 30,000 feet overview of construction process so that we know what to measure. As aforementioned analysis is based on SBP report, third section shows how SBP data is arrived at. The fourth section asks us to empathize with SBP as it is under immense pressure. The fifth section reviews the recent news on the projects that have registered for amnesty to glean valuable data that will help with the analysis. The sixth section is where we put the understanding we gained in the first 5 parts to revisit the BR graph that was presented in the beginning of this blogpost that sent us down this rabbit hole. Finally, we finish off with how to go about analyzing the impact of construction package. I do hope you enjoy it.

Section 1: How not to design a construction package

This section will present the summary of the construction package. For those interested in detailed analysis, they can read the below article.

To qualify for the amnesty, which comprises of 1) no questions asked about source of funds and 2) a flat tax rate (effectively negligible) based on the size of the unit, the developer/builder has to register the project with FBR by Dec 31, 2020 and complete the project by September 30, 2022 (21 months to completion). There are four criteria and one can claim amnesty by qualifying under any criterion.

- Criterion 1: For construction of building, completion is defined as grey structure to be complete.

- Criterion 2: For housing society, completion is defined as 50% of the plots sold and of the sold plots, buyers should have paid 40% of purchase price of plots.

- Criterion 3: For buyers of units in these projects, no questions asked about source of funds if full payment for purchase made by Sep 30, 2022.

- Criterion 4: Those who already own a housing units, can sell the housing units without paying capital gains tax on it.

Criterion 1 is the only one that is promoting construction, if any. Criterion 2 is absurd as it is promoting a plot culture. All that is required under this criterion is to sell 50% of plots and receive 40% payment of those plots and voila money is whitened and effective tax becomes negligible. Criterion 3 can act as incentive for construction i.e. if the buyer decides to buy an apartment constructed under criterion 1 thus providing additional impetus to the builder to construct and deliver that unit. Criterion 4 seems to be an attempt by the advisors of the construction package to minimize their own taxes i.e. these are already constructed and owned housing units. This one doesn’t even pretend to be related to construction. A question should be asked from the bureaucrats and advisors who designed this package why is this one included as part of the construction package. Who is getting relief under criterion 4? Thus, three out of the four criteria of the construction package don’t even promote construction.

The additional wrinkle in the amnesty is that it requires 21 month to complete the project as those projects that are not completed by Sep 30, 2022 will be disqualified. Small buildings or plotting (throughout this post, I will refer to plot selling schemes as plotting) can be completed in such a short time but a high rise may require a longer time to achieve the project completion milestone i.e., grey structure is completed. It was evident from day 1 when the ordinance was introduced in April that extensions may be necessary for completion date. Ridiculous to introduce conditions in a package which everyone knows won’t be satisfied and extensions will be required. Only those projects that are targeting criterion 2 i.e plotting can confidently achieve completion by expiry date. By introducing such a near term completion date, the package is implicitly discouraging construction.

Calling it a construction package is a misnomer. It should be called a money laundering/tax minimization/plotting package.

Criterion 3 requires full payment for the purchase of the unit to be made by September 2022 ie in 21 month. If the builder decides to build something for the buyers who want to qualify under criterion 3, not many people have funds equivalent to full price of apartments ie Rs.70 lakh+ lying around except those who have hidden sources of wealth. For such buyers, it is better to build a high-end apartments. Criterion 3 encourages building of high end apartments which does nothing to fill the housing requirement of the population. For the people who are buying these 2 crore and 3 crore apartments, they weren’t feeling the shortage of housing anyway. In addition, there is a limit to how many high end apartments these people want to invest in considering that rental yields in Pakistan are very low.

The below ad makes it clear what type of apartments this amnesty is promoting. The price starts from Rs.3 crore and that was May 2020.

Criterion 3 provides an incentive to the builder to target the higher end of the market and higher end is significantly smaller than what majority of the population needs. Thus criterion 3 implicitly discourages large scale construction for the masses by not incentivizing construction for them.

This is why I call this construction package a lesson in how not to design a construction amnesty scheme. Earlier, I also did a deeper dive in how not to design a diaspora bond when the government launched Pakistan Banao Certificate (predecessors of Naya Pakistan Certificate) to bypass approaching IMF.

Section 2: Construction Financing Process

This gives a brief overview of high rise construction. Cost of the project can be divided into land cost and construction cost (for the sake of simplicity we are assuming soft costs such as architecture costs, municipal charges, approval and permit charges are all included in construction cost). Land usually comprises 25% of project cost with construction cost comprising balance 75%. Banks in Pakistan don’t finance land and limit their financing to around 50% of the total cost of the project i.e. 50% of loan-to-cost (LTC). If a builder wants to finance a building, he will have to arrange money to purchase the land. Plus he will also arrange another 25% for carrying out initial construction cost. Once the builder has financed 50% of the project from his own sources (equity, borrowing from friends, family, associates, purchaser deposits etc), then the bank will start financing balance of the cost. The bank will not hand over the 50% loan amount in lump sum. Instead the bank will receive a monthly report from Quantity Surveyor of how much work has been done that month and will release only that amount of the loan.

Let’s take an example. Assume cost of high rise is Rs.1 billion. 25% land cost means the construction cost is Rs.750 million. Say it will take 3 years to construct the building from the date excavation is started. Thus, every month approximately Rs.21 million construction cost will be incurred on project (Rs.750 million construction cost / 36 months). If the bank is financing at 50% LTC, it means bank will only finance the final Rs.500 million of the project. The builder will have to arrange the initial Rs.500 million from own sources: the builder will initially pay Rs.250 million for the land. Then he will pay Rs.21 million every month towards construction for the next 12 month bring the total cost incurred on the project to Rs.500 million. When the 50% milestone is achieved, now the bank will enter the picture. As stated above, the bank will not hand over Rs.500 million to complete the project. Rather bank will release only Rs.21 million. In the next month, Quantity Surveyor will present a report to the bank that Rs.21 million that was disbursed last month has been used in the project as required. Then the bank will release the next instalment of Rs.21 million. This is done to minimize leakage i.e. prevent the builder from diverting the bank’s loan for non-project related costs.

Section 3: SBP Reporting

This blogpost started with graph based on SBP data showing increase in construction loans. How does this report get generated? Let me take you behind the scenes.

SBP does not have an online access to the database of the banks to see how banks are performing day to day. Each bank is running its own banking system and banking system of one bank may be completely different from another bank and from SBP. At the end of the month, each bank generates an Excel sheet consisting of the data required by SBP in the format required by SBP. SBP compiles all the Excel sheets, sums up the data and reports it on its website showing the performance of the bank. SBP does not audit this report every month unless there is something that stands out as extraordinary. It has been years since I worked on this report so the system may have changed to where SBP will provide automatic forms etc but the bottom line remains that SBP data is based on reports prepared by the banks.

How do banks prepare this report? Do they update every time a loan is disbursed which industry it is going to? In most cases, no. When a borrower opens an account with the bank, the borrower is assigned an industry classification. Thereafter, every loan that is provided to that borrower is shown as going to that industry even if the purpose of the borrowing is unrelated to it. This is not a big deal as most borrowers usually borrow for their own industry and a single loan by a borrower for a different purpose by a won’t sway the overall industry data in a meaningful way.

To give an example, in 2005, I marketed and booked Crescent Steel and Allied Products Limited (CSAPL). It was very profitable at the time. When we created the account in our banking system, we showed it as a steel manufacturer. At the time, there steel business wasn’t making much money and all the profit they were making was from their trading activity in stock market. We also provided them a loan of, I think, around Rs.100million to trade in the stock market. When the month end reporting went to SBP, it showed that funds are being provided to a steel manufacturer. If research houses and business press is monitoring the SBP data, they will report that steel manufacturing is in expansion mode or their working capital requirements are increasing. Similarly, if CSAPL requests us to finance their setting up of a PVC pipe manufacturing facility as now they are experts in pipes, we are not going to update in our outdated system that this new loan is going for a PVC factory and not a steel factory (unless it’s a completely different borrowing entity).

This why the title of the SBP report is Advances by Borrower (industry classification) and not what is the specific purpose of the advance. The loan given to borrower to set up a PVC pipe factory is being reported as loan given to a steel pipe manufacturer.

Section 4: SBP under pressure

SBP is one of the better managed public institutions in the country but those who have been following me on twitter know that I have some issues with them. Now I have toned down my rants as I realized that SBP especially SBP governor is under pressure after royally screwing up the economy in attracting hot money. The pressure is obvious from the below two stories.

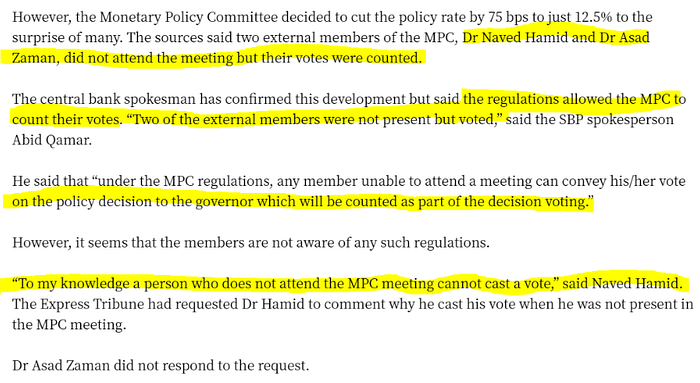

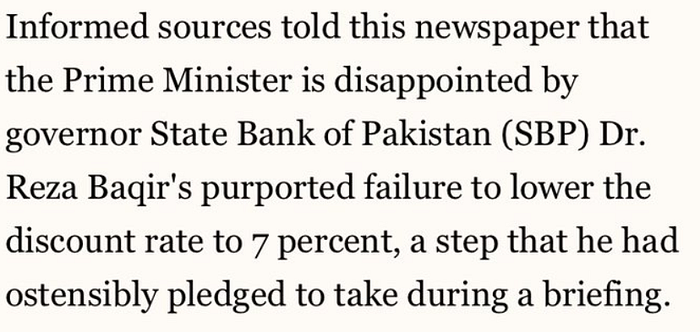

One, when he had to reduce the discount rate. Based on the metrics that SBP follows namely inflation and economists that SBP governor keeps close to him, the interest rate should not have been reduced. But SBP governor was under immense pressure from PM to reduce the rates. Thus despite the fact that there wasn’t enough quorum in the MPC meeting, he reduced the rates. Occasionally newspapers get it wrong but this time the newspaper reached out to the two absent members and they were shocked that how votes were cast on their behalf without their consent and knowledge.

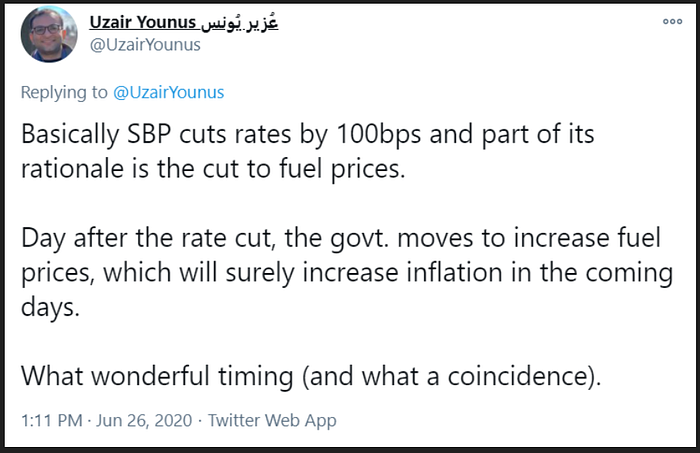

This was followed by another stunt in June.

PM irked by non-compliance of his directives? — Business Recorder (brecorder.com)

The justification of the rate cut

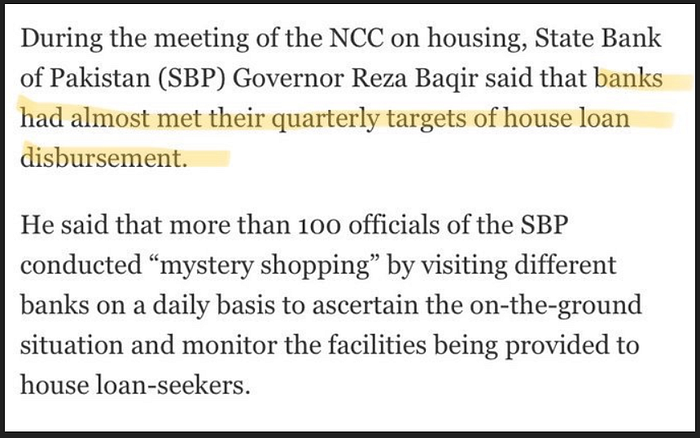

Two, in a recent meeting with PM, SBP governor said that banks are meeting the mortgage financing target and this is further substantiated by SBP staff of 100 making visits to various branches of commercial banks as “mystery shoppers”. The very next day, Pakistan Banking Association sends out a circular to all the banks lamenting that banks are not giving out mortgages as per target. The same information is also visible in SBP data which implies that banks are encouraging their staff to take out mortgages. This shows that SBP governor is not only telling “safaid jhoot” to the face of PM but he is also adding flourishes to it by adding details like “mystery shoppers”. This begs the question is it only the governor lying or rot has spread downwards that even mystery shoppers are lying to please the governor. All this lying appears ridiculous when SBP’s own data shows banks aren’t lending to consumers. Oh well…

Work on Ravi urban project has started, PM told — Pakistan — DAWN.COM

People have high hopes from SBP Governor. He is young, smart, Aitchisonian, has a PhD and has worked at IMF. The purpose of this part was to show that SBP Governor is feeling the heat to show that steps taken by him are helping the government achieve its manifesto promises. Thus any statements by SBP and especially SBP governor should be taken with a pinch of salt.

The post I wrote of steps taken by SBP if anyone is interested in my views about SBP

Section 5: Construction package data as announced in the news

I have mentioned earlier that the money laundering package was a masterclass in how not to design a construction package. Apparently, the reason amnesty was only allowed till December 31, 2020 was because IMF was against it and only relented when the Dec 31, 2020 was set as last date of registration. As the deadline for the amnesty approached, the stakeholders (my guess is it is mainly ABAD with their undeclared money) started stirring the pot to get an extension on the scheme. Just try to keep track of the numbers that were shared in the last 5 days. The date are dates of the newspaper so the event being reported took a day before.

December 26

In the meeting with PM, a request was made to him to extend package by six months as a quite a few developers could not get the necessary approvals in place and it was stated that extension would lead to additional 1.3 trillion worth of projects getting registered. As is the trend in Pakistan, messages were also sent around on WhatsApp.

December 28

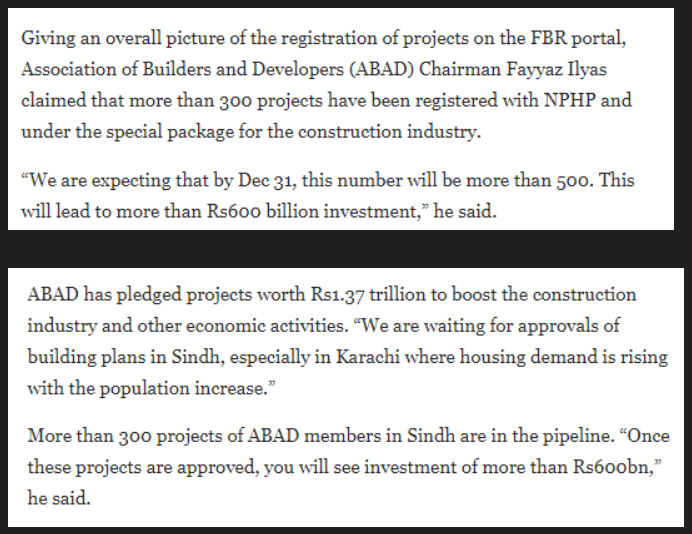

ABAD and its members including current and previous chairman have been making outrageous and unsubstantiated claims about housing since this government took over but as those claims are music to the ears, no one questions them. I have a done a few threads on those. Anyway, ABAD chairman says by Dec 31 (3 days from now) 500 projects will be registered with FBR under the scheme with total project value of Rs.600 billion and further reiterates the Rs.1.37 trillion claim.

Then the Chairman ABAD goes overboard and says NAPHDA is guaranteeing approvals of loans on the commercial bank from these projects. NAPHDA is guaranteeing no such thing.

In addition, I am also not sure how banks will treat this with the sword of FATF hanging over them. Will they want to finance a project which is being constructed using laundered money?

Needless to mention, we don’t know how many of the proposed 500 projects are high rise schemes and how many are plot schemes. Always safe to assume that 25% of the Rs.600 billion cost is land cost.

December 29

One day later (and two days before year end), only 350 projects registered so far with total size of rupees 140 billion.

Let’s unpack this. Going from Rs.140 billion existing project to Rs.1.37 trillion is an increase of almost 10x. Are there 10x projects in the pipeline? Does ABAD even have the capacity to manage this many projects? I doubt it.

Secondly, more than half of the projects are existing projects i.e., if we are measuring the impact of the amnesty package as how much new construction it is incentivizing, then the impact of amnesty package is only half of what is being counted above. So instead of 10x in the pipeline, we should ask, are there 20x projects in the pipeline and do they even have the capacity to execute them.

Builders are very smartly is registering their existing ongoing projects under the amnesty scheme that they were completing anyway with or without the amnesty scheme. The policy was devised in consultation with builders and there is a reason they call this next best thing after independence. Thus the builder is minimizing his taxes proportionally and get money laundering amnesty on existing projects that they were completing anyway while also gaining brownie points with the PM saying “boss aap nay amnesty di, hum nay project deliver kia”. The PM and the government will make the statement in their press releases that amnesty package is delivering. The newspapers and research houses will publish reports praising the package. No one will be wiser.

Did you notice the the hyperbole of ABAD chairman? Till 3 days ago, we was boasting that total projects worth Rs. 600 billion will be registered by Dec 31. However, projects registered to date are valued at Rs.140 billion and projects not registered to date are Rs. 125 billion i.e. total of Rs.265 billion against ABAD chairman’s claim of Rs.600 billion.

Needless to mention, we do not know how many of the Rs.140 billion are existing projects and how many of the both registered and future projects are plot schemes. Also safe to assume, 25% of the project costs will be land cost.

December 31

One day till the deadline.

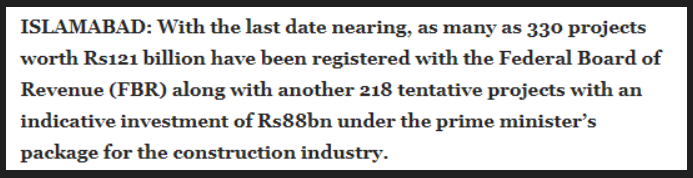

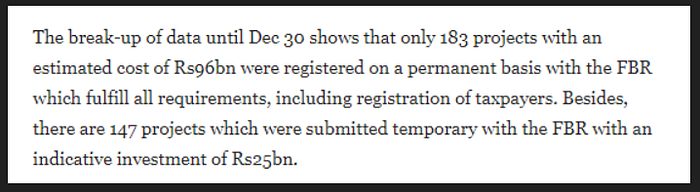

In a matter of 5 days, we have gone from Rs. 600 billion to 265 billion to 209 billion. Of this only projects of Rs.121 billion have completed formalities. Even of this 121 billion, 96billion are registered on permanent basis while other 25 are registered on temporary basis.

Needless to mention, we do not know how many of these projects are existing projects and how many are plotting schemes.

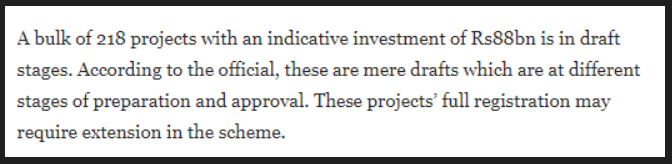

And remember that claim of due to non-extension of scheme, Rs.1.37 trillion of projects are stuck. Well this is the real size of those projects.

From Rs.1.37 trillion to Rs.88 billion. Is there no one that will ask them what is going on?

Below is an additional tidbit that we weren’t considering earlier

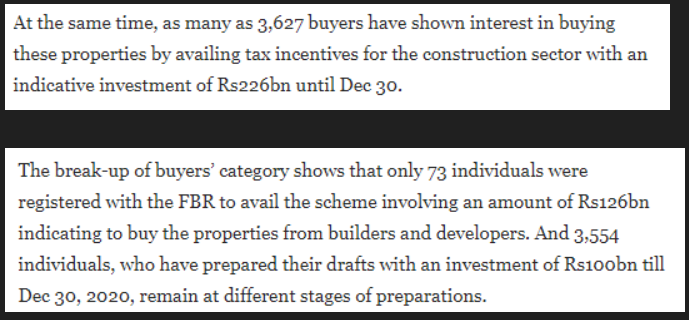

The total size of the projects under amnesty both registered as well as in draft state are for Rs.209 billion whereas there are buyers reportedly with Rs.227 billion of undeclared wealth looking to purchase the units. Now if these builders build what these buyers want, the builders will not require any financing from the bank to complete the projects. These ultra-wealthy and cash rich can make the payment to builder to complete the construction by September 2022. If analysts are looking at bank financing to measure whether construction due to the amnesty package is taking off, they will be under reporting the utilization under the construction package as the builder’s borrowing isn’t a true reflection of efficacy of construction package.

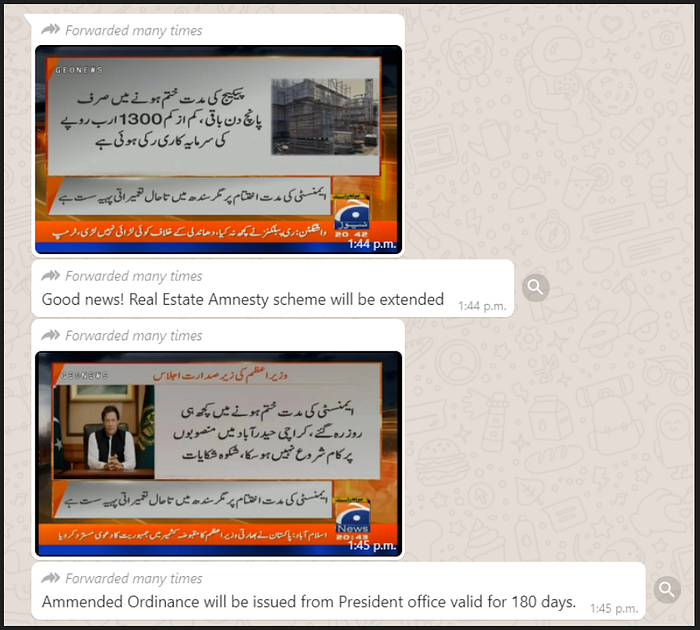

January 1

PM announces 6 month extension in the construction package both in the registration date as well as completion date.

From Rs.121 billion registered till a day before as per FBR, the number of registered projects went up to Rs.186 billion as quoted by PM who is also quoting FBR. The pending projects went up from Rs.88 billion Rs.116 billion.

We are truly living in a post truth world. I do not know which number to go with. Needless to mention, we do not know how many of these are existing projects and how many are plot schemes. Do not forget that approximately 25% of the project cost is land cost.

The PM also said that this will lead to increase in economic activity of Rs.1.5 trillion in Punjab and I will leave it to research houses and financial press to quote professional economists justifying it. I am not a professional economist.

The one take away of this section is don’t believe a word of what comes out of Kamran Khan, AKD, and real estate affiliated professionals when it comes to impact of the amnesty package on the economy.

One aspect which I didn’t emphasize but should be evident is the amnesty package incentivizes overstating the cost of the project. Higher the cost stated, higher will the money that is whitened and lower will be taxable income and if these developers are whitening 100s of billions of undeclared income, it goes without saying that they will be expert in over invoicing.

Section 6: Bringing it all together analyzing the analysis

My teacher of Quranic Arabic used to advise us when he was teaching us rules of Quranic grammar to think of the rules as tools in your tool kit. Next time when we read Quran, we should use the tools to analyze the ayaats. Similarly, I like to think that the background I have provided above provides the readers of this post with tools to analyze real estate sector. Let’s revisit the news that was in the beginning of this page.

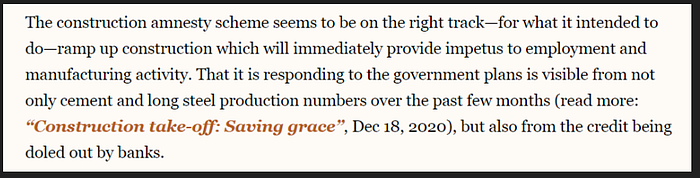

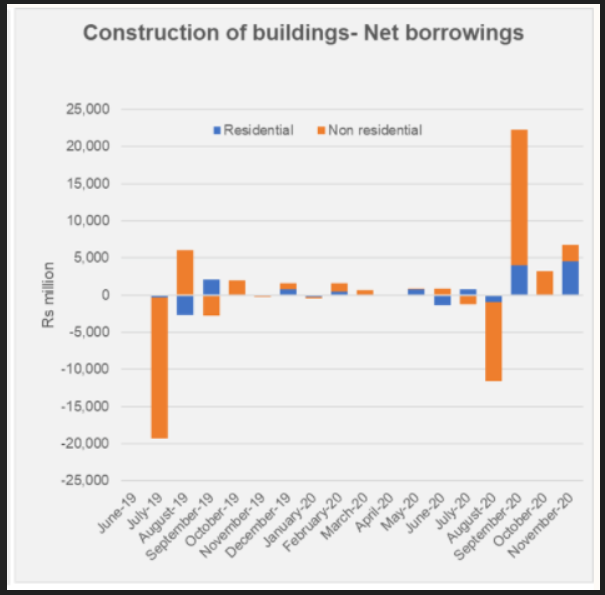

The newspaper says that impact of amnesty is visible from credit doled out by the bank. If you look at the non-residential segment, it went from zero or negative borrowing to a borrowing of Rs.23 billion in the month of September.

As we know, banks do not provide lump sum financing for a project rather provide financing as work progresses. Are we saying that from no activity for more than a year, the construction sector completed 23 billion of construction in a single month? Someone should check what is happening here. However, if it helps to sell the narrative that amnesty package is working as planned, its high fives all around and it is in no one’s interest to verify that number.

Let’s play it safe and just use the loans doled out for residential construction in September i.e. Rs.4 billion. For the amnesty project, let’s take the number for registered projects (highly suspect) that was presented by PM i.e. Rs.186 billion. We know that half of the projects are existing projects which means that only Rs.93 billion worth of projects will have reached a stage that they will be in a position to borrow. The balance new projects would still be in a stage where they are trying to achieve 50% project cost contributed so cannot borrow from the bank (assuming banks are lending at 50% LTC). We are also assuming all these 93 billion projects are high rise projects otherwise they will not qualify to borrow as banks usually do not lend for plotting. Assuming a 36 month average construction period gives a monthly loan request of Rs.2.5 billion (this is assuming work is continuing on all the existing projects). We see that residential lending for month of September is Rs. 4 billion which is 60% higher than what is the maximum possible that can be borrowed due to amnesty package. We made some aggressive assumptions here and still the number isn’t reconciling. We are also assuming that banks lend for construction to everyone but the fact of the matter is banks only lend to limited number of builders like Trakker, Dolmen, Lucky, Arif Habib etc (that is why ABAD chairman was making the ridiculous statement that NAPHDA is guaranteeing an approval of loan by banks 4 days ago). Based on this, we can rest assured that whatever is causing an increase in construction lending, amnesty package has nothing to with it. We can also conclude lending by banks to construction sector is absolutely the wrong metric to judge whether the construction amnesty is working.

The analysis also claims that increase in cement and steel production show construction amnesty is working. Are we sure? If using aggressive assumptions, the maximum amount amnesty construction sector could borrow in a month is Rs.2.5 billion while September’s actual borrowing for construction sector was Rs.23 billion. This sector will be gorging on steel and cement as most like their requirements for raw material are 10x the size of amnesty sector. We can also conclude, for now, that production or consumption cement and steel are the wrong metrics to judge the amnesty.

Concluding Section: How to analyze the impact of construction amnesty?

Is there no way to measure the impact? There is. But it may not be possible to do desk research on it. It will require field work. First we need to get the details of the project that have been registered with FBR both existing as well as new. With respect to existing projects, judgment call may be required whether to include them as project that would not have been completed if amnesty hadn’t been announced. Identify the high rise projects (as those are the only one where construction activity will take place). Select a representative sample of the projects of both types (existing and new), visit the sites and note the status of their construction. By visiting the sites periodically, we can estimate how the construction is progressing and how much construction has happened. FBR data will tell us what is the estimated cost of the project (highly overstated but what can you do). Seeing the percentage of progress of construction, one can estimate how much construction cost is being incurred due to the amnesty package. The analyst may not have to visit the sample projects himself. Any up and coming real estate brokerage house will do the work (and even provide drone footage if needed) for a nominal fee.

Conclusion

It is improbable (if not impossible) that we will be able to estimate the impact of amnesty scheme based on publicly available data. However, some rolling up the sleeves and fieldwork can enable us to estimate if the package has delivered the desired results. Some steps to keep in mind

- The cost of the projects will be overstated

- Usually 25% of the project cost is land cost. This can change or may have already changed. There are exceptions too.

- Only high rise will lead to increase in type of construction that is the objective of the amnesty i.e. 40 related industries, job growth and increase in housing stock.

- Try to exclude, if possible, existing projects i.e. those projects that the builder was already completing with or without the amnesty.

- Finally, don’t believe any of the numbers that are being thrown by AKD, Kamran Khan, ABAD and there associates when it comes to construction activity taking place.

Bonus Features

I am sorry if the above was not what you were looking for. As such, I have added this bonus feature.

As you can see, nobody is interested in calculating or verifying the actual impact of construction package and even SBP is dying to report increase in construction activity, if somehow you work in a bank and are having a tough time meeting the construction lending targets set by SBP (if it comes to that) or want to earn brownie points with the government, below based on my experience, how you can achieve the construction lending targets if push comes to shove. First rule of innovative thinking in corporate world. Always CYA.

1. Review the clients who are borrowing for any construction activity. For example, it could be a trading client who is borrowing money for building its new headquarters. If the borrowed money is significant, it is the judgment call of the bank what qualifies as significant, change the industry classification of the borrower from a trader to construction because as far as the bank is concerned, the borrower is engaged in construction activity. The overall lending position of the bank remains the same but it’s loans doled out for construction suddenly increase. SBP won’t object and the government will be more than pleased with the bank.

2. If you have a construction client that the risk committee refused to finance earlier because he was asking for unreasonably cheap money and he is now building with his own money and his project is say 80% complete. With the blessing of your risk committee, request him to borrow money from you at very cheap rates. If you are providing 50% LTC, it means 30% of the loan goes out on day 1 instead of the trickling 2% every month. This helps you achieve construction loan disbursement target at a low risk. Though you may not be making as much money as you would like, but if you are seeking some brownie points from SBP or the government, this loan deployment will help you achieve those for a slightly lower interest rate that is not too steep a price.

If you like this blogpost, you may also like my last blogpost on the rise and fall of shadow banking in India.

Amazing rise and spectacular fall of shadow banking in India | by 2paisay | Dec, 2020 | Medium